The chart of accounts is a list consists of all accounts that are used in the company’s general ledger. The accounting software application will use the chart of accounts to arrange information into the company’s financial statements such as the Balance Sheet and the Profit and Loss. The chart is arranged in order according to the account numbers so that it is easier to locate certain accounts. The account numbers could be numeric or alphabetic, or both, alphanumeric.

Usually, the accounts are arranged in order in the financial statements, start with the balance sheet and next, the income statement (Also see What You Need to Know About Record Keeping). Therefore, the chart of accounts begins with cash, continues with liabilities and shareholder’s equity, then proceed through accounts for revenues and expenses.

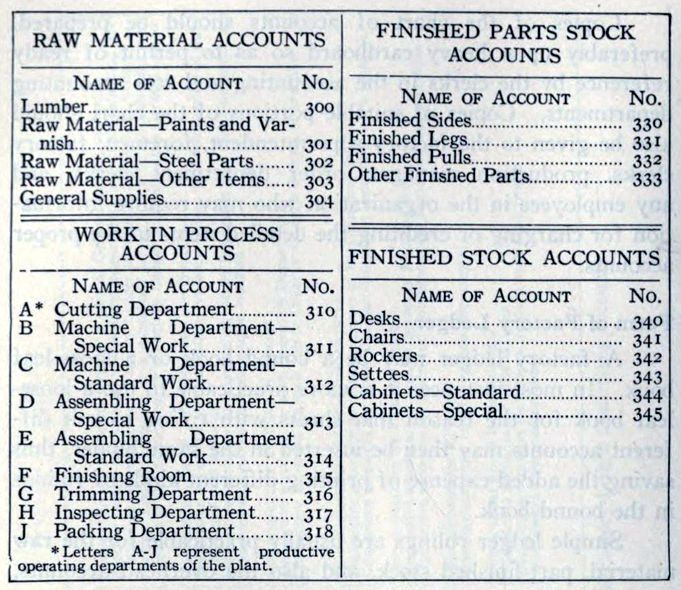

Numerous companies have structured their chart of accounts to enable the expenditure info is separated according to the different department; therefore, the engineering department, accounting department, and sales department would have the same expense accounts set. The setup of the chart of accounts depends on the requirements of the specific business.

Accounts in the chart of accounts:

- Assets:

- Cash (main bank account)

- Cash (payroll account)

- Marketable Securities

- Petty Cash (Also see Importance of a Petty Cash Book)

- Allowance for Doubtful Accounts

- Accounts Receivable

- Fixed Assets

- Prepaid Expenses

- Accumulated Depreciation

- Inventory

- Other Assets

- Liabilities:

- Notes Payable

- Accounts Payable

- Taxes Payable

- Accrued Liabilities

- Wages Payable

- Shareholders’ Equity:

- Retained Earnings

- Preferred Stock

- Common Stock

- Revenue:

- Revenue

- Allowances and sales returns

- Expenses:

- Bank Fees

- Cost of Item Sold

- Payroll Tax Expense

- Advertising Cost

- Supplies Expense

- Utility Cost.

- Depreciation Cost

- Rent Cost

- Wages Cost.

- Other Expenses

Best Practices for Chart of Accounts

- Reduce the size of the accounts.

Examine the account list regularly to check if there are irrelevant quantities in the accounts. If so, and if these details are not required for unique reports, close down these accounts and roll the kept information into a bigger account. Doing this regularly could reduce the number of accounts so that it is easier to manage them.

- Consistency.

It is essential to produce a chart of accounts that would probably not change for the next few years, as you can compare the results of the same account over a few years. However, if you begin with a little number of accounts and then

If you start with a small number of accounts and after that slowly increase the number of accounts, it would end up being very difficult to get comparable financial details for more than the previous year.

- Lockdown.

Do not let subsidiaries to alter the standard chart of accounts without significant reason. This is because it would be harder to consolidate the outcomes of the business if you have numerous versions.

If you still have any queries about the chart of accounts, do not hesitate to get an accounting service in Singapore for more guidance for your company.